The Energy Report: Uranium hit lows this summer before recovering somewhat, although the uranium price is still well below the highs of several years ago. Would you discuss the fundamentals for uranium and your predictions for the price over the next several years?

Ross McElroy: We saw the spot price of uranium hit a multiyear low of about $18 per pound ($18/lb) in late November/early December 2016. But we've also seen, in the short period from the beginning of December up until currently in March, the spot price recover to close to $25/lb. That represents a price increase of about 40% over just a few months. Of course, $25/lb is still a very low price.

At the low end, the major low-cost producers, primarily the Kazakhstan producers and Cameco Corp. (CCO:TSX; CCJ:NYSE), one of the world's largest uranium producers, sent signals to the market—by reducing low-cost production and shutting in higher-cost production—that they're not selling uranium any cheaper than that. Those are among the lowest-cost producers worldwide. It has gotten to a point where even they can't make any money. There's no profit margin left, even for those with the lowest cost production.

I think that we've seen a bottom in the price of uranium. When we look at the costs of production around the world to bring on new mines or even get the majority of the ones that are already operational to be profitable, we're going to have to see uranium prices increase substantially closer to $50–60/lb. And to bring on any meaningful new production, prices need to be closer to $60–70/lb. So even from where uranium is at right now, a huge improvement in price is needed to go forward.

We know the demand is there. The reactor build-out worldwide continues to increase. The most significant, of course, is the acceleration of the build-out of reactors in China. China currently gets about 2% of its energy needs by nuclear power. Its goal is to raise that level to around the 15 to 20% range. That means China is going to have to build out another 150 to 200 or so reactors. That's an incredible growth story just on its own. But it's not the only country that's on that trajectory. India also has significant growth plans and even the Middle East is increasing its use of nuclear power.

We only have to go out 10 to 15 years to see electricity demand growing by 150%, with nuclear being a significant part. It's my expectation that, within the next two years or so, we'll see substantial increases in the price of uranium, perhaps getting closer to $40–50/lb as discussed. That's how I see the near-term horizon.

TER: At the end of February, Fission Uranium Corp. (FCU:TSX; FCUUF:OTCQX; 2FU:FSE) released drill results that discovered a new area of mineralization as well as an extension of both ends of its mineralized trend. Just a few weeks later you hit wide mineralization in the same area and you have the start of a new, high-grade zone. Can you tell us more about these results?

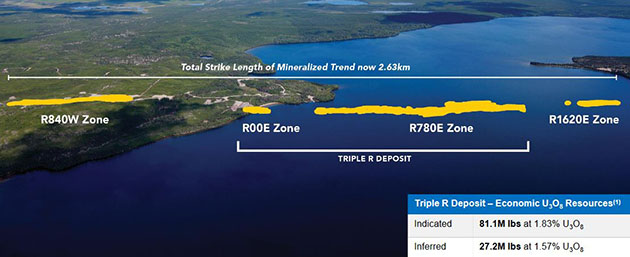

RM: We were very pleased with our first results from our latest batch of drilling. When we stepped out around 600 meters (600m) along the same mineralized trend that already hosts our Triple R uranium deposit, which is the world's most significant high-grade shallow deposit, we encountered significant anomalous radioactivity with counts up to 3,200 counts per second. In the world of measuring radioactivity—which ultimately translates to uranium—that's significantly anomalous. We felt that we were close to high-grade mineralization, stepping out on our exploratory plan along the Patterson Lake South (PLS) corridor trend. We know that that trend should continue for significant distance both to the east and the west. It's a great big, long conductive trend that already hosts two world-class uranium deposits (Fission's Triple R and NexGen's Arrow) and indications of others (Cameco's Spitfire zone). And as we stepped out 600m to the west of our R840W zone, we were seeing signs of a new area of potential for us.

A good part of the thrust of our winter program is to make a new discovery. We're looking for the next Triple R deposit. We followed up that big stepout hole with another seven holes, five of which intersected anomalous radioactivity over a 180m strike length. Included in this was hole PLS17-539, which is approximately 510m west of our large, high-grade and shallow zone called R840W. We hit 31m of continuous mineralization, including high-grade radioactivity. This is a great result for us because we have a strong track record of really growing these new zones and you just have to look at the Triple R, which is composed of two zones, and the additional zones on either side of our deposit that we have not yet added to our resource estimate.

Thanks to this new zone our mineralized strike length is now 3.14km—the largest in the Athabasca Basin region. Growing the zone is going to be our clear focus going forward, but we have no intention of stopping there. PLS is a remarkable project and we have a number of other exploration hot spots that we are pursuing.

TER: You mentioned that the Triple R is the world's highest-grade shallow deposit. How important is it that the deposit is shallow? What does that mean for your costs?

RM: The Triple R deposit is not the biggest deposit in the world; it's also not the highest grade, although it ranks up there with some of the biggest highest-grade deposits, which is really what the Athabasca Basin is famous for. What really sets Triple R apart from everything else is its shallow nature. The top of our deposit starts at around 50m below surface, and we've been able to delineate that to about 300m depth. So it's very shallow.

What shallow means is that this is open pittable. And there are no other open-pit potential deposits of this size and grade anywhere in the world. All the other high-grade deposits in the Athabasca Basin region are deeper. And deep deposits can often represent much more of a challenge to develop. For one thing, deep underground mining is generally more expensive to mine. Deep underground uranium mines take a great deal of specialty engineering in order to mine the ore.

An open pit is a much simpler type of mine plan. That's what really makes this deposit unique. We can put an open pit in the ground and access the ore more quickly because it's near surface. A rule of thumb in mining is, with all things being equal, the shallower the deposits are, the more economically viable they tend to be because they're less expensive and less technically challenging to get out of the ground. That's what really sets our deposit apart from everything else.

TER: Fission announced that it is increasing its winter drill program, adding 29 holes. What do you hope to accomplish this winter?

RM: The increase in the drill program was primarily so that we could add a much larger exploration component to the drilling. We have a two-pronged approach this winter.

Part of what we're doing is growing the newly discovered high-grade pods on the west and east sides of the Triple R deposit. Those two pods, known as 840W and 1620E, are not yet part of a resource estimate. We believe that with enough holes to delineate them, we can potentially bring them into a resource estimate and thus grow the Triple R deposit by pounds.

PLS is a very large property that's just rife with exploration targets. This winter we are putting a greater emphasis on hunting for the next occurrence of high-grade mineralization that we hope is just around the corner. We already talked about the discovery 600m to the west; that's part of our push to have a greater emphasis on exploration. If we can make another discovery and find an entire new deposit either on trend or on a parallel trend, that will be a meaningful and material event for the company. The additional 29 holes are primarily a really hard look at exploration.

TER: When you expect to finish this drilling and get assay results?

RM: The winter drilling window in the Athabasca typically starts in January, and it's very much weather dependent. Once spring comes and the snow and ice start to melt, that usually signals that the program has to come to an end. We expect that the drilling will continue until mid-April. So we have about another month to go in the program.

Assays follow, typically for us, about six weeks after drilling. So there's usually a six-week lag time from drilling a hole to when we see the assays from the lab.

You will start seeing assay news flow probably in the next two weeks, and it should continue into late May.

TER: When do you expect to release a resource estimate and a prefeasibility study (PFS)?

RM: I mentioned the goal is basically to bring our newly discovered high-grade zones, the 840W and the 1620E, into the overall resource estimate. To do that, we still probably need another drill program. That'll be this summer's program, which would start in July and go until September. So I suspect we're looking at a resource estimate toward the late fall/early winter, so November/December of this calendar year. That's our goal.

A PFS might be the next step. We released a preliminary economic assessment (PEA) in 2015. The next step is possibly to move directly into a PFS. We could have that put together by, say, H1/18 if we so choose. That would mean we'll have to do a little more engineering work in the field, some geotechnical holes and a bit more metallurgical studies. Those are necessary components of the PFS.

We're already very advanced in other important areas. We know the resource itself is robust enough. As 75% of our resource is Indicated, our drilling is sufficient on the main zone to do an advanced PFS study. That resource data set is good. So we have to pin down a little more on the engineering side to advance to a PFS. Thus possibly in 2018 we could look for a PFS.

TER: Where do you see Fission going from here?

RM: On the PLS project, as I mentioned, there are a couple of prongs that we want to take. On the advanced project side, we want to develop the Triple R deposit, grow the resource by adding in the new zones and move the project forward through prefeasibility and eventually down the road into feasibility to a point where a production decision can be made. We think that this project has a great chance of being a producer. Our PEA study indicates that Triple R could potentially be a very low-cost producer.

On the blue-sky side, the whole western side of the Athabasca Basin is an underexplored area. Our property is a large package right in the heart of this prospective western Athabasca region. Because it's such a large land package that's virtually underexplored, we think there's a lot of potential to find other occurrences of high-grade deposits on the property.

Part of our approach will be to look for new occurrences and also to bring what we already know further up the food chain, closer to the eventual production decision. That's a multiyear approach for both aspects.

TER: If the price of uranium stays low, what would Fission's strategy be?

RM: We're very mindful of the uranium price. We saw the very low prices in 2016 at close to $18. When we weren't sure when the price was going to turn around, we started to pull in the reins, finding ways to reduce our general and administrative costs.

Fission is an exploration company, which means the majority of its spend is exploration. And for us, that's discretionary spending. It's not money that we have to spend to keep the property in good standing, and it's not like having an operating mine where there are costs associated with shutting in or just inactivity. For us, if we have a low uranium price market, we just reduce our costs. We don't have the requirement to spend that money to explore, but we have the option to do so.

Having said that, shareholders stand behind Fission because we are successful at what we do and we are an aggressive company, and we're very nimble with the sense of the market. If the uranium market looks like it's picking up, we increase our spending.

This winter's program is a real reflection of that. We were prepared to reduce spending on our exploration significantly this winter. And then once we had the budgets approved, the uranium market picked up, things were exciting and the share price increased. So we felt the opportunity was there to actually expand our program.

We're quite nimble. It's up to us to read the market and try to make those decisions. But it's a fairly easy and straightforward process for us to either turn down spending or dial it up accordingly. So if it's a low price market, we'll continue to watch our spend and make sure that we don't burn through the significant treasury that we have.

TER: Any parting thoughts for our readers?

RM: We think that a turnaround in the uranium market has already occurred. We've seen the price of the commodity, at least on the short-term spot market, increase by about 40%.

Share prices of uranium companies are leveraged to the price of uranium. In that time frame, Fission is up around 60%. So we had a low that coincided with the low price of uranium. Our share price was $0.50. We're around $0.80 now. Our share price has increased at a rate greater than the increase in the price of uranium.

Good companies have leverage to increase in share value as the price of the commodity goes up. We believe that uranium is on an upward trajectory. But more importantly than anything is it will be a select number of companies that have really good, meaningful, low-cost assets such as our Triple R deposit that turn around to the greatest degree.

The market is changing. Investors should have another look at uranium. There are pretty compelling reasons why they would want to invest in the sector, and then they should look to Fission as being the cream of the crop of companies to pick.

TER: Thanks for your insights.

Ross McElroy, president, COO and chief geologist of Fission Uranium Corp. is a professional geologist with nearly 30 years of experience in the mining industry. He is the winner of the PDAC 2014 Bill Dennis award for exploration success and the Northern Miner "Mining Person of the Year 2013." He has comprehensive experience with working and managing many types of mineral projects from grassroots exploration to feasibility and production.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you'll learn when new interviews and articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Articles page.

Disclosure:

1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or her family owns, shares of the following companies mentioned in this interview: None.

2) Fission Uranium Corp. is a sponsor of Streetwise Reports. Streetwise Reports does not accept stock in exchange for its services. Click here for important disclaimers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security.

3) Fission Uranium Corp. had final approval of the content and is wholly responsible for the validity of the statements. Opinions expressed are the opinions of Ross McElroy and not of Streetwise Reports or its officers.

4) Ross McElroy: I was not paid by Streetwise Reports to participate in this interview. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. I or my family own shares of the following companies mentioned in this interview: Fission Uranium Corp.

5) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts' statements without their consent.

6) This interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports' terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports.

7) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.